Embarking on the journey to buy a new home represents a significant life milestone, promising the creation of lasting memories and the establishment of a personal sanctuary. This endeavor, while thrilling, involves numerous options and critical decisions, necessitating a clear, strategic approach from the outset. A successful home acquisition hinges on meticulous planning, from establishing a realistic budget to navigating complex financial instruments and legal processes. This comprehensive guide aims to illuminate each phase of the homebuying process, transforming what can often feel like an overwhelming undertaking into an enriching and confident experience.

I. Getting Financially Ready

The foundation of a successful home purchase lies in a robust understanding of one’s financial standing and the various monetary commitments involved. This initial phase equips prospective homebuyers with the essential knowledge and tools necessary before they even begin house hunting.

A. Deep Dive into Budgeting: Beyond the Price Tag

A truly comprehensive financial plan extends beyond the initial purchase price and down payment. While many homebuyers focus on these immediate figures, a thorough understanding of the total cost of homeownership is paramount for long-term financial stability. This includes not only the principal and interest of a mortgage but also property taxes and homeowner’s insurance, collectively known as PITI. Overlooking these ongoing expenses, along with other significant costs such as closing fees—which typically range from 3-6% of the total purchase price and encompass various fees and taxes —can lead to unexpected financial strain.

For instance, failing to account for private mortgage insurance (PMI), required when less than a 20% down payment is made, adds to monthly expenditures. Similarly, ongoing maintenance, utilities, and potential homeowners association (HOA) fees are vital components of a realistic budget. A robust budget, therefore, is not merely about securing a loan; it is about establishing a sustainable foundation for homeownership. This comprehensive approach helps individuals avoid a common pitfall: underestimating the true financial commitment of buying a home.

The strategic planning of a down payment also plays a crucial role in shaping the financial landscape of homeownership. The amount contributed as a down payment directly influences the type of loan available, the presence of mortgage insurance, and ultimately, the interest rate secured. For example, while some government-backed loans offer as little as 0% down, conventional loans typically require 3-20%. A larger down payment can significantly reduce a lender’s perceived risk, potentially leading to a more favorable interest rate. This connection between the down payment and loan terms underscores that the down payment is not just a lump sum payment, but a strategic decision with long-term financial implications. By understanding this dynamic, buyers can optimize their financial comfort and make a wise investment.

B. Mastering Mortgage Pre-Approval: The Non-Negotiable First Step

Obtaining mortgage pre-approval is a critical early step in the homebuying process, moving beyond a mere financial check to become a strategic market advantage. Pre-approval signifies a lender’s conditional commitment to provide a loan, based on a detailed review of an applicant’s financial profile, including a “hard credit check”. This rigorous vetting process distinguishes pre-approval from pre-qualification, which is a preliminary estimate based on self-reported financial data.

For sellers, a pre-approval letter serves as tangible proof that a prospective buyer is serious and financially capable, granting a competitive edge in a bustling market. Without this documentation, offers may not be taken seriously, potentially leading to missed opportunities. The pre-approval process typically involves submitting extensive financial documentation, and the resulting letter is generally valid for 30 to 90 days. This timeframe provides buyers with a clear budget within which to shop, enabling them to act quickly and decisively when an ideal property is identified. The ability to present a pre-approval letter empowers buyers, transforming the often-emotional process of house hunting into a more confident and streamlined experience.

C. Navigating Mortgage Options: A Guide to Loan Types

Understanding the diverse landscape of mortgage options is essential for tailoring financing to individual circumstances and financial goals. Beyond simply knowing current mortgage rates, prospective homebuyers must explore the various loan types available, each with distinct eligibility criteria, down payment requirements, and interest rate structures.

The primary categories of home loans include:

- Conventional Loans: These are the most common type of mortgage, often requiring a credit score of 620 or higher and down payments ranging from 3% to 20%. While they can be more challenging to obtain than some government-backed options, they often result in lower overall costs. Conventional loans are further categorized into conforming loans, which adhere to Federal Housing Finance Agency (FHFA) standards, and non-conforming loans (jumbo loans), designed for higher-value properties.

- Government-Backed Loans: These programs are designed to make homeownership more accessible to specific groups or in particular areas.

- FHA Loans: Insured by the Federal Housing Administration, FHA loans are known for their lower credit score requirements, sometimes as low as 500 with a 10% down payment, or 580 with 3.5% down. They offer broad eligibility without location or income restrictions. However, FHA loans require mortgage insurance premiums, which add to monthly costs.

- USDA Loans: Guaranteed by the U.S. Department of Agriculture, these loans target moderate- to low-income borrowers in eligible rural and some suburban areas. A significant benefit is the potential for 0% down payment for many qualified homebuyers, often with less expensive mortgage insurance fees compared to FHA loans. USDA loans typically require a minimum credit score of 620 and are exclusively offered as 30-year fixed-rate loans.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, VA loans are available to eligible veterans, servicemembers, and surviving spouses. A key advantage is the possibility of a 0% down payment.

Beyond the loan type, the interest rate structure is another critical consideration:

- Fixed-Rate Mortgages: These loans maintain the same interest rate throughout the entire loan term, ensuring stable monthly principal and interest payments. Common terms are 15 or 30 years. This option is generally preferred by borrowers planning to remain in their home for an extended period.

- Adjustable-Rate Mortgages (ARMs): ARMs begin with a lower, fixed introductory interest rate for a set period (e.g., 5 years for a 5/6 ARM), after which the rate adjusts periodically based on market conditions. ARMs can be advantageous for borrowers who anticipate moving or refinancing before the fixed-rate period expires.

The choice of mortgage type is highly individualized, influenced by factors such as credit score, down payment availability, debt-to-income ratio, and long-term residency plans. Understanding these nuances allows buyers to select the financing that best aligns with their unique financial situation and future aspirations, avoiding the common pitfall of only consulting a single lender or overlooking government-backed programs.

Table 1: Key Mortgage Types Comparison

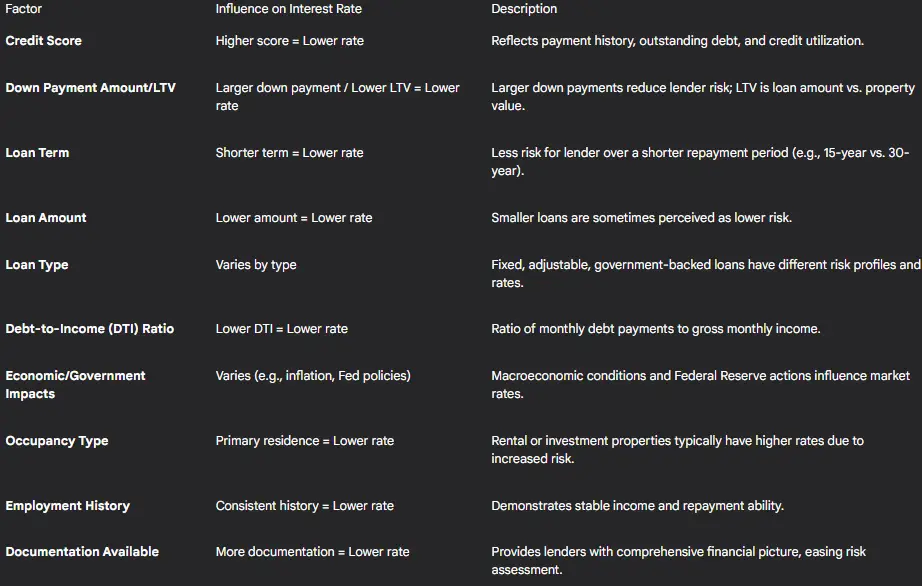

Several factors beyond the loan type itself can significantly influence the interest rate a homebuyer receives. These include personal financial health and broader economic conditions. A higher credit score, for example, typically translates to a lower interest rate, as it signals lower risk to lenders. Similarly, a larger down payment, which results in a lower loan-to-value (LTV) ratio, often leads to more favorable rates because it reduces the lender’s exposure. The loan term also plays a role; shorter terms (e.g., 15-year mortgages) generally have lower interest rates than longer terms (e.g., 30-year mortgages) due to the reduced risk over a shorter repayment period.

Economic indicators such as inflation, the job market, and Federal Reserve policies also exert considerable influence on mortgage rates, causing them to fluctuate. A lower debt-to-income (DTI) ratio, which reflects a healthy balance between monthly income and debt obligations, can also contribute to securing a lower interest rate. Understanding these interconnected variables empowers homebuyers to optimize their financial profile and make informed decisions that can lead to substantial savings over the life of the loan.

Table 2: Factors Influencing Your Mortgage Interest Rate

D. Unlocking Down Payment Assistance Programs: State and Local Opportunities

For many aspiring homeowners, particularly first-time buyers, the hurdle of a substantial down payment can seem insurmountable. However, numerous down payment assistance (DPA) programs exist at state and local levels, offering crucial financial aid that can make homeownership a reality. These programs often provide deferred-payment junior loans or grants to help cover down payments and/or closing costs.

Eligibility for these programs typically includes being a first-time homebuyer, intending to occupy the property as a primary residence, completing mandatory homebuyer education counseling, and meeting specific income limits. Examples include California’s CalHFA MyHome Assistance Program, which can offer up to 3-3.5% of the purchase price or appraised value, and New York City’s HomeFirst Down Payment Assistance Program.

The existence of these programs represents a significant, yet often underutilized, resource. Many individuals mistakenly believe that homeownership is out of reach due to insufficient savings for a down payment. By actively investigating and leveraging these assistance programs, buyers can overcome this common financial barrier. The application process typically begins by contacting a HUD-approved counseling agency, which can guide applicants through eligibility requirements and help them obtain the necessary certificates. This proactive approach transforms a perceived financial limitation into an actionable pathway to homeownership, directly addressing the fundamental question of “How much money do I need?”.

II. Finding Your Ideal Property

Once financially prepared, the next phase involves translating budgetary parameters and personal aspirations into identifying the perfect living space and community. This requires a thoughtful approach that balances immediate desires with long-term needs.

A. Refining Your Home Vision: House vs. Home

The distinction between a “house” and a “home” is more than semantic; it is fundamental to finding a property that truly resonates with one’s lifestyle and aspirations. While a house is a mere structure of walls and beams, a home is a space that reflects personality, values, and dreams. A critical aspect of this discernment involves looking beyond superficial aesthetics, such as shiny countertops or cozy fireplaces, and instead focusing on the less visible, yet equally vital, aspects.

This means evaluating the layout, design, and functionality to ensure the space effortlessly adapts to daily routines and supports a desired quality of life. A home should not merely meet current needs but possess the potential to evolve with a lifestyle over the years. Considering future needs, such as potential family growth, the integration of remote work spaces, or aging-in-place considerations, transforms the property selection process from an immediate gratification exercise into a strategic, forward-thinking investment. Failing to consider these long-term implications can lead to regret or the necessity for costly renovations or moves in the future. By embracing this broader perspective, buyers can ensure their chosen property is not just a comfortable abode, but a wise investment that aligns with their long-term financial well-being and personal fulfillment.

B. Strategic Neighborhood Selection: Beyond Location

The adage “location, location, location” holds profound truth in real estate, extending beyond mere geographical placement to encompass lifestyle, community, and even financial considerations. Selecting the right neighborhood is as crucial as choosing the house itself, as it sets the stage for the chapters of one’s life to unfold. This involves a comprehensive assessment of priorities, determining whether a quiet suburban haven, a bustling urban hub, or a close-knit community best aligns with individual preferences.

Beyond the general ambiance, a thorough evaluation of surrounding amenities is paramount. This includes proximity to quality schools, parks, shopping districts, entertainment venues, and essential healthcare facilities. The daily experiences and conveniences offered by a neighborhood significantly contribute to overall satisfaction with a new home. To truly grasp the “soul” of a community, engaging with locals and exploring neighborhood events can provide invaluable insights into its character.

Furthermore, a strategic approach to neighborhood selection involves considering its dynamic nature and investment potential. Exploring “up-and-coming areas” can reveal hidden gems that balance lifestyle preferences with affordability. Crucially, prospective buyers should research the “future growth potential” and “resale value” of an area. A neighborhood with strong growth prospects can lead to property appreciation, reinforcing the idea that a home is not just bricks and mortar, but an investment in a lifestyle and a financial asset. Conversely, neglecting these long-term factors can result in dissatisfaction or diminished resale value. This holistic approach to neighborhood selection helps buyers avoid the common pitfall of fixating solely on the house while overlooking the vital context of its surroundings.

C. Assembling Your Expert Team: Roles of Key Professionals

Navigating the complexities of homebuying is significantly streamlined by assembling a trusted team of professionals. These individuals collectively form an interconnected support system, guiding buyers through each stage of the process, mitigating risks, and ensuring a smoother transaction.

- Real Estate Agent: An indispensable ally, a real estate agent possesses an intimate understanding of local market trends, including pricing dynamics, inventory levels, and neighborhood specifics. They have access to a vast array of listings, including properties not publicly available, and can efficiently sift through options to pinpoint homes matching specific criteria. Beyond identifying properties, agents offer strategic guidance, from crafting competitive offers to adeptly negotiating prices, repairs, and contingencies. They act as an objective intermediary, particularly valuable in emotionally charged negotiation phases. Furthermore, a knowledgeable agent helps buyers navigate the legalities of contracts and disclosure requirements and provides crucial emotional support throughout what can be an exciting yet apprehensive journey. A seasoned agent also brings a professional network of lenders, inspectors, appraisers, and attorneys, streamlining various stages of the buying process.

- Loan Officer vs. Mortgage Broker: These financial professionals play distinct yet complementary roles in securing a mortgage.

- A Loan Officer is employed by a specific bank, credit union, or mortgage lender, offering only the loan products and rates available from that institution. They guide borrowers through the application process, assist with pre-approval, and prepare closing documents. Working with a loan officer means direct interaction with the entity funding the loan, which can be beneficial for those with unusual financial situations.

- A Mortgage Broker, on the other hand, is an independent intermediary who collaborates with multiple lenders to find the best mortgage product and rates tailored to a borrower’s financial situation. Brokers can help determine qualifications, gather necessary documentation, and sometimes negotiate fees with lenders. The key distinction lies in their scope: loan officers are limited to one lender’s offerings, while brokers provide access to a wider range of options from various institutions.

- Real Estate Attorney: While not required in all states, a real estate attorney provides critical legal protection and guidance throughout the home purchase. Their primary role is to safeguard a client’s interests, ensuring a clean title to the property by performing thorough title searches for hidden claims, liens, or ownership issues. Attorneys review and draft all necessary contracts, including the purchase agreement, ensuring fairness and clarity, and explaining complex legal terms. They navigate legal complexities such as property lines, zoning regulations, or easements. In many jurisdictions, attorneys also facilitate the closing process, managing final paperwork, ensuring correct fund transfers, and recording the deed. Should disputes arise, a real estate attorney is equipped to negotiate, mediate, or even litigate on behalf of their client.

Engaging a skilled and collaborative team of professionals from the outset is paramount. Hesitating to ask for information or clarity from these experts can create significant problems as the transaction progresses. The collective expertise of this team ensures smoother transactions, better deals, and reduced legal and financial risks, empowering buyers to navigate the complexities of homebuying with confidence.

III. The Offer, Inspection, and Appraisal

After identifying a potential home, the subsequent phases involve critical evaluations and strategic negotiations to ensure the property’s value and condition align with the buyer’s investment and expectations.

A. Crafting a Competitive Offer: Negotiation Tactics and Contingencies

Submitting an offer on a home initiates a crucial negotiation phase, often likened to a strategic game where each move can significantly impact the outcome. Crafting a competitive offer goes beyond merely stating a price; it involves a nuanced understanding of market conditions and strategic negotiation tactics. Real estate agents play a vital role in this stage, helping buyers determine a fair yet compelling offer based on comparable sales in the area.

The negotiation process is typically a back-and-forth exchange where sellers may accept, reject, or counter an offer. However, negotiation extends far beyond the sale price. It encompasses critical terms and contingencies, such as potential repairs, upgrades, and specific conditions that protect the buyer’s interests. Contingencies—like those related to home inspection, financing approval, or appraisal—are crucial clauses that allow a buyer to withdraw from the contract without penalty under predefined circumstances. These clauses are vital risk mitigation tools, safeguarding the buyer against unforeseen issues.

A common pitfall for homebuyers is allowing emotions to dictate decisions, leading to overpaying for a property or stretching beyond their financial means. Maintaining objectivity and adhering strictly to a pre-established budget is essential for making sound financial decisions. A skilled negotiator, often guided by their real estate agent, leverages market knowledge and strategic planning to secure the best possible deal, not just in terms of price, but in overall terms and conditions, thereby ensuring a financially sound acquisition.

B. The Indispensable Home Inspection: What It Covers, What It Doesn’t, and How to Respond to Findings

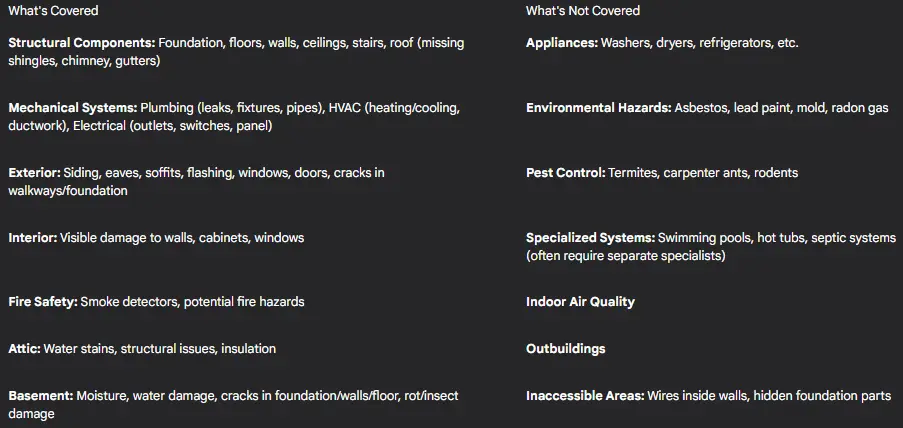

The home inspection is a non-negotiable step in the homebuying process, serving as a critical due diligence imperative rather than an optional expense. Neglecting a thorough inspection is a common mistake that can lead to significant, costly hidden issues down the road. This comprehensive safety and quality assessment, typically conducted by a licensed inspector, is designed to uncover existing or potential problems with the property.

A standard home inspection covers readily visible and accessible parts of a home, both interior and exterior. This includes structural components such as the foundation, floors, stairs, walls, ceilings, and the roof (checking for missing shingles, damaged chimneys, or clogged gutters). Mechanical systems are also thoroughly examined, including plumbing (checking for leaks, functioning fixtures, and pipe condition), HVAC systems (heating and cooling operation and ductwork), and electrical systems (outlets, switches, light fixtures, and the circuit breaker panel). Inspectors also look for signs of water or fire damage, visible mold, and safety elements like smoke detectors and railings. The inspection typically occurs within 10 to 30 days after an offer is accepted and costs roughly $300-$500.

However, it is equally important to understand what a standard home inspection does not cover. These exclusions often include appliances (like washers and dryers), indoor air quality, environmental hazards such as asbestos, lead paint, mold, or radon gas, outbuildings, swimming pools, and pests (e.g., termites, rodents). Additionally, inaccessible or hard-to-reach areas, like electrical wires inside walls or certain parts of the foundation, are typically not inspected. If concerns exist in these excluded areas, scheduling separate evaluations by certified specialists is advisable.

D. Unlocking Down Payment Assistance Programs: State and Local Opportunities

For many aspiring homeowners, particularly first-time buyers, the hurdle of a substantial down payment can seem insurmountable. However, numerous down payment assistance (DPA) programs exist at state and local levels, offering crucial financial aid that can make homeownership a reality. These programs often provide deferred-payment junior loans or grants to help cover down payments and/or closing costs.

Eligibility for these programs typically includes being a first-time homebuyer, intending to occupy the property as a primary residence, completing mandatory homebuyer education counseling, and meeting specific income limits. Examples include California’s CalHFA MyHome Assistance Program, which can offer up to 3-3.5% of the purchase price or appraised value, and New York City’s HomeFirst Down Payment Assistance Program.

The existence of these programs represents a significant, yet often underutilized, resource. Many individuals mistakenly believe that homeownership is out of reach due to insufficient savings for a down payment. By actively investigating and leveraging these assistance programs, buyers can overcome this common financial barrier. The application process typically begins by contacting a HUD-approved counseling agency, which can guide applicants through eligibility requirements and help them obtain the necessary certificates. This proactive approach transforms a perceived financial limitation into an actionable pathway to homeownership, directly addressing the fundamental question of “How much money do I need?”.

II. Finding Your Ideal Property

Once financially prepared, the next phase involves translating budgetary parameters and personal aspirations into identifying the perfect living space and community. This requires a thoughtful approach that balances immediate desires with long-term needs.

A. Refining Your Home Vision: House vs. Home

The distinction between a “house” and a “home” is more than semantic; it is fundamental to finding a property that truly resonates with one’s lifestyle and aspirations. While a house is a mere structure of walls and beams, a home is a space that reflects personality, values, and dreams. A critical aspect of this discernment involves looking beyond superficial aesthetics, such as shiny countertops or cozy fireplaces, and instead focusing on the less visible, yet equally vital, aspects.

This means evaluating the layout, design, and functionality to ensure the space effortlessly adapts to daily routines and supports a desired quality of life. A home should not merely meet current needs but possess the potential to evolve with a lifestyle over the years. Considering future needs, such as potential family growth, the integration of remote work spaces, or aging-in-place considerations, transforms the property selection process from an immediate gratification exercise into a strategic, forward-thinking investment. Failing to consider these long-term implications can lead to regret or the necessity for costly renovations or moves in the future. By embracing this broader perspective, buyers can ensure their chosen property is not just a comfortable abode, but a wise investment that aligns with their long-term financial well-being and personal fulfillment.

B. Strategic Neighborhood Selection: Beyond Location

The adage “location, location, location” holds profound truth in real estate, extending beyond mere geographical placement to encompass lifestyle, community, and even financial considerations. Selecting the right neighborhood is as crucial as choosing the house itself, as it sets the stage for the chapters of one’s life to unfold. This involves a comprehensive assessment of priorities, determining whether a quiet suburban haven, a bustling urban hub, or a close-knit community best aligns with individual preferences.

Beyond the general ambiance, a thorough evaluation of surrounding amenities is paramount. This includes proximity to quality schools, parks, shopping districts, entertainment venues, and essential healthcare facilities. The daily experiences and conveniences offered by a neighborhood significantly contribute to overall satisfaction with a new home. To truly grasp the “soul” of a community, engaging with locals and exploring neighborhood events can provide invaluable insights into its character.

Furthermore, a strategic approach to neighborhood selection involves considering its dynamic nature and investment potential. Exploring “up-and-coming areas” can reveal hidden gems that balance lifestyle preferences with affordability. Crucially, prospective buyers should research the “future growth potential” and “resale value” of an area. A neighborhood with strong growth prospects can lead to property appreciation, reinforcing the idea that a home is not just bricks and mortar, but an investment in a lifestyle and a financial asset. Conversely, neglecting these long-term factors can result in dissatisfaction or diminished resale value. This holistic approach to neighborhood selection helps buyers avoid the common pitfall of fixating solely on the house while overlooking the vital context of its surroundings.

Table 3: Home Inspection Checklist: What’s Covered & What’s Not

If the inspection report reveals significant problems, the buyer is not without recourse. The findings can provide powerful leverage for negotiation or even an exit strategy from the purchase. Options include requesting a price decrease or a credit on the purchase price to cover the cost of necessary repairs, asking the seller to undertake the repairs themselves (often by contracting professionals), or, in cases of severe or numerous issues, choosing to withdraw from the purchase entirely. This protective aspect of the inspection reinforces its value as a crucial step in making an informed and financially sound homebuying decision.

C. Understanding the Home Appraisal: Valuing Your Investment and Addressing Discrepancies

The home appraisal is an essential component of the homebuying process, serving as an independent, unbiased assessment of a property’s fair market value. Its primary purpose is to protect the lender’s interests by ensuring that the loan amount requested is justified by the home’s actual worth. This dual function also implicitly safeguards the buyer from overpaying for a property.

The lender typically orders the appraisal, but the borrower is usually responsible for paying the fee, which generally ranges from $300 to $550. The appraisal process involves a licensed or certified professional conducting a visual inspection of the home and analyzing comparable sales in the neighborhood and current market conditions. Key factors evaluated by an appraiser include the home’s general condition, age, and quality of materials, its location (considering views, school district ratings, and proximity to public transportation), lot size, square footage, number of bedrooms and bathrooms, and any significant upgrades or improvements.

A critical situation arises if the home’s appraised value comes in lower than the agreed-upon purchase price. In such cases, the mortgage lender will not lend more than the appraised value. This discrepancy necessitates a re-evaluation of the deal. Buyers have several options: they can attempt to renegotiate the purchase price with the seller to match the appraised value, make up the difference in cash, or, if an agreement cannot be reached, potentially withdraw from the contract if an appraisal contingency is in place. If a buyer disagrees with the appraisal, they can request the lender to revisit the assessment through a process called a Reconsideration of Value (ROV). This understanding of the appraisal’s role and potential outcomes empowers buyers to navigate financial challenges that may arise, reinforcing the strategic nature of the “Deal or No Deal” phase.

IV. Closing the Deal and Beyond

The final phase of the homebuying journey culminates in the official transfer of ownership, followed by the transition into life as a homeowner. This stage requires careful attention to detail and an understanding of the various costs and legal documents involved.

A. Demystifying Closing Costs: A Detailed Breakdown

Closing costs represent a significant financial obligation, typically ranging from 3-6% of the total purchase price, and are comprised of various fees and taxes due at the time of closing. These costs can vary based on the loan type and the property’s location. Understanding who pays what is crucial, as responsibilities are determined by the purchase contract and local practices.

Generally, the buyer is responsible for costs related to obtaining the mortgage and securing the property. These commonly include application fees, appraisal fees, attorney fees, document and courier fees, inspection fees, lender fees (such as loan origination and title insurance for the lender), property taxes (often prorated), recording fees, survey fees, and transfer taxes.

Sellers, on the other hand, typically cover expenses related to transferring ownership and commissions. These often include real estate agent and broker commissions (which can be 5-6% of the home’s price), agreed-upon repairs, prorated property taxes, seller attorney fees, title insurance (for the owner’s policy), and transfer taxes.

Escrow fees are another common component of closing costs. Escrow refers to a protected account overseen by a neutral third party that holds funds from both the buyer and seller until the property ownership officially changes. These fees, which can be a flat rate (around $500-$2,000) or up to 1% of the purchase price, cover the administration of the account, fund transfers, notary charges, and photocopying. While often split 50/50 between buyer and seller, the allocation of escrow fees is ultimately subject to negotiation within the purchase agreement.

A key aspect often overlooked by first-time homebuyers is that closing costs are “always open to negotiation”. Buyers can strategically ask sellers to contribute towards these costs, especially if the seller is motivated to finalize the deal. Lenders may also offer discounts on their service fees as an incentive. This understanding transforms closing costs from a fixed, unavoidable expense into a potential area for financial savings, allowing buyers to proactively optimize their financial outlay and avoid underestimating the total costs involved.

Table 4: Common Closing Costs: Buyer vs. Seller Breakdown

B. The Critical Role of the Title Company and Escrow Officer

The roles of the title company and escrow officer are fundamental to ensuring a secure and legally sound transfer of property ownership. While often operating behind the scenes, these entities act as crucial neutral third parties, safeguarding the interests of both buyer and seller and facilitating a smooth transaction.

A title company’s primary responsibility is to ensure that the property being sold has a “clear and marketable title,” meaning it is free of any liens, encumbrances, or legal issues that could affect ownership. This is achieved through a meticulous

title search, an in-depth review of public records to confirm legal ownership and identify any potential “clouds” on the title, such as unpaid taxes, property liens, or past legal actions like foreclosures. The results are compiled into a preliminary title report, which serves as a commitment for title insurance.

Following the title search, the title company issues title insurance policies. An owner’s title insurance policy protects the buyer from future claims or disputes over ownership, offering vital protection against financial loss if a title defect emerges years after closing. A lender’s title insurance policy, typically required by the mortgage provider, protects the lender’s investment.

Beyond title services, title companies commonly provide escrow services. In this capacity, they act as an escrow officer, holding all funds (such as the buyer’s earnest money deposit and loan proceeds) and documents (like the signed deed) securely until all conditions of the sale are met. Funds and documents are only disbursed according to the written instructions of both the buyer and seller, ensuring a fair and protected transaction. The title company also plays a central role in

document preparation and recording, drafting and reviewing essential closing documents—including the deed, settlement statement, and loan documents—and ensuring their accuracy and compliance with local regulations. After closing, they are responsible for recording the deed and mortgage with the county land records office, formally registering the new ownership.

The meticulous work of title companies and escrow officers forms the bedrock of secure ownership transfer. Their thorough processes prevent costly surprises and delays that could jeopardize the transaction. This detailed attention to legal and financial integrity provides peace of mind, reinforcing that the investment in a home is not just in a physical structure, but in a legally protected asset and a secure future.

C. Closing Day: The Final Steps to Homeownership

Closing day marks the culmination of the homebuying journey, the moment when property ownership is officially transferred to the buyer. This event typically occurs four to eight weeks after an offer is accepted, allowing ample time for inspections, appraisals, and securing financing.

On closing day, several key actions take place: funds held in escrow are transferred to cover various costs, the buyer provides mortgage and title fees, the deed of the house is updated to the buyer’s name, and all necessary legal papers are signed by both buyer and seller. The meeting often involves the buyer, seller, their respective attorneys, bank or lender representatives, and potentially real estate agents.

A multitude of documents are reviewed and signed, each playing a critical legal and financial role:

- Deed/Property Transfer Forms: These are the legal documents that formally transfer ownership from the seller to the buyer.

- Affidavit of Title (Seller’s Affidavit): A legal statement by the seller confirming their ownership, that no other parties are buying the property, and that there are no undisclosed liens against it.

- Mortgage/Deed of Trust: This document legally secures the home as collateral for the loan, outlining the lender’s right to foreclose if loan terms are violated.

- Promissory Note: A formal legal statement where the borrower agrees to repay the mortgage lender, detailing the loan amount, interest rate, payment schedule, and terms of default.

- Closing Disclosure: This form provides a comprehensive breakdown of all financial details of the mortgage, including loan terms, projected monthly payments, and total closing costs. It is crucial to receive and review this document at least three business days before closing.

- Initial Escrow Statement: Details how property taxes, homeowners insurance, and other prepayments will be managed through the escrow account.

- Flood Insurance Disclosure: Provides information regarding the requirement or option to purchase flood insurance based on the property’s location.

To ensure a smooth closing, buyers should bring essential items such as all closing paperwork, a government-issued photo ID, proof of homeowners insurance (which lenders mandate), and a cashier’s or certified check for closing costs. A final walk-through of the property shortly before closing is also highly recommended to ensure it is in the expected condition and that any agreed-upon repairs have been completed. The closing process, while intense due to the volume of paperwork, represents a meticulous legal and financial culmination. Thorough review of all documents beforehand helps prevent errors and future roadblocks, ensuring a secure and confident transition into homeownership.

D. Avoiding Common Homebuyer Pitfalls: Lessons Learned and Proactive Strategies

While the homebuying journey is exciting, it is also fraught with potential pitfalls that can lead to stress, financial strain, or regret. Recognizing and proactively addressing these common mistakes is crucial for a positive and successful experience.

One of the most frequent errors is ignoring the budget by underestimating the total costs involved, particularly ongoing expenses beyond the initial purchase price. This often stems from a lack of understanding of PITI and other hidden costs. A proactive strategy involves creating a comprehensive budget that accounts for all potential expenditures, including property taxes, insurance, maintenance, and HOA fees, and adhering to guidelines like the 28% rule for mortgage payments.

Another significant mistake is skipping mortgage pre-approval before beginning the house hunt. Without a clear understanding of buying power, individuals risk falling in love with homes they cannot afford, and sellers may not take their offers seriously. The solution is to obtain pre-approval early, which provides a realistic budget and enhances credibility as a buyer.

Many buyers also err by focusing solely on aesthetics, neglecting crucial long-term considerations like the neighborhood’s suitability, future growth potential, or resale value. A more effective approach involves thorough neighborhood research, considering factors such as schools, commute times, and community amenities, and envisioning how the property will evolve with future needs.

Neglecting the home inspection is another costly oversight, often done to save money. This can lead to the discovery of expensive hidden issues after purchase. Investing in a comprehensive inspection is a small cost compared to the potential pitfalls it can prevent, and its findings can provide valuable negotiation leverage.

Rushing the process is a mistake that can lead to quick decisions and subsequent regret. Taking ample time to research neighborhoods, compare listings, and negotiate terms ensures a more considered and confident purchase. Similarly,

hesitating to ask questions or seek clarity from real estate professionals can create misunderstandings and problems. Buyers should feel empowered to ask for all necessary information.

Furthermore, being careless with credit between pre-approval and closing can jeopardize final loan approval. Opening new credit accounts, making large purchases, or closing existing accounts can negatively impact a credit score. Maintaining financial stability during this period is paramount.

Talking to only one lender is another common pitfall, as it can mean missing out on potentially better rates or loan terms. Shopping around with multiple lenders can lead to significant savings.

Finally, overlooking government-backed loans (FHA, VA, USDA) can lead buyers to assume they have no financing options, especially if they have a low down payment or less-than-perfect credit. Exploring these programs can open doors to homeownership that might otherwise seem closed. Additionally,

making decisions based purely on emotion can lead to overpaying or stretching beyond financial means. Maintaining a practical, budget-driven approach is key to avoiding emotional attachment to a home that is not yet secured.

By understanding these common pitfalls and adopting proactive strategies—such as adhering to a realistic budget, securing pre-approval, thoroughly researching neighborhoods, investing in comprehensive inspections, taking a measured approach, asking questions, protecting credit, and exploring all financing options—homebuyers can significantly enhance their journey, making it smoother, less stressful, and financially sound.

V. Key Recommendations and Next Steps

The journey to homeownership, while complex, becomes navigable and rewarding with a strategic, informed approach. The comprehensive insights discussed herein underscore the importance of preparation, due diligence, and leveraging expert guidance at every turn.

For prospective homebuyers, the following actionable steps are recommended:

- Prioritize Financial Readiness: Begin by establishing a holistic budget that accounts for all costs of homeownership, not just the purchase price. Secure mortgage pre-approval early to clarify buying power and strengthen offers in a competitive market. Thoroughly research and compare various loan types, including government-backed options, to find the best fit for individual financial circumstances. Actively investigate state and local down payment assistance programs, as these can significantly reduce upfront financial burdens.

- Define Your Home and Neighborhood Vision: Look beyond superficial aesthetics to identify a property that aligns with long-term lifestyle needs and has the potential to evolve. Conduct in-depth research into neighborhoods, considering not just amenities and culture, but also future growth potential and resale value.

- Assemble a Professional Team: Engage a trusted real estate agent, a knowledgeable loan officer or mortgage broker, and a diligent real estate attorney. These professionals provide invaluable market insights, negotiation expertise, legal protection, and guidance through complex processes.

- Exercise Due Diligence: Approach the offer, inspection, and appraisal phases with meticulous attention. Craft competitive offers that include protective contingencies. Invest in a comprehensive home inspection and understand its scope, using findings as leverage for negotiation or as a basis for reconsideration. Understand the appraisal process and be prepared to address any discrepancies between appraised value and purchase price.

- Prepare for Closing: Demystify closing costs by understanding the breakdown of buyer and seller responsibilities and recognizing areas for negotiation. Familiarize oneself with the critical roles of the title company and escrow officer in ensuring a clear title and secure fund transfer. Prepare thoroughly for closing day by reviewing all documents in advance and understanding the final steps.

- Learn from Common Pitfalls: Actively avoid common mistakes such as underestimating costs, skipping pre-approval, focusing solely on aesthetics, neglecting inspections, rushing decisions, being careless with credit, or failing to explore all financing options.

For ongoing content maintenance and promotion of this guide, the following suggestions are crucial:

- Regular Content Updates: Consistently review and update property listings, market trends, and financial information within the guide to maintain accuracy and relevance for search engines and users.

- Continuous SEO Monitoring: Regularly monitor keyword performance, organic traffic, and user engagement metrics (e.g., click-through rate, bounce rate) to adapt and refine the content strategy.

- Enhance Local SEO: Ensure the Google My Business profile is optimized with accurate NAP information, high-quality photos, and actively managed client reviews to boost local search visibility and build trust.

- Strategic Promotion: Leverage social media platforms and email marketing campaigns to disseminate the updated guide, reaching a broader audience of prospective homebuyers.

- Content Diversification: Consider developing supplementary content formats, such as short videos explaining complex mortgage types, interactive infographics detailing closing costs, or virtual tours of sample homes, to further engage users and enhance the guide’s utility.

By adhering to these recommendations, the homebuying process can be transformed from a daunting challenge into a fulfilling and financially sound journey, leading individuals to a place where dreams unfold and memories blossom.

Follow us on Facebook for the latest Radvin Group news or contact us to get the best investment offers

What is mortgage pre-approval and how long is it typically valid?

Mortgage pre-approval is a lender’s conditional commitment to provide a loan after a detailed financial review and hard credit check. It is generally valid for 30 to 90 days.

What are the main types of mortgage loans available to homebuyers?

The main types of mortgage loans include Conventional, FHA, USDA, VA, Fixed-Rate, and Adjustable-Rate Mortgages (ARMs).

What factors can influence the interest rate a homebuyer receives on a mortgage?

Factors influencing mortgage interest rates include credit score, down payment amount, loan term, loan amount, loan type, debt-to-income (DTI) ratio, economic conditions, occupancy type, and employment history.

What is the role of a real estate agent in the homebuying process?

A real estate agent provides market knowledge, access to listings, strategic guidance, negotiation skills, helps navigate legalities, offers insightful advice, and provides emotional support throughout the homebuying journey.

What does a standard home inspection cover?

A standard home inspection covers readily visible and accessible parts of a home, including structural components, plumbing, HVAC, electrical systems, and the roof, assessing for damage and proper functioning.

What is a home appraisal and who typically orders and pays for it?

A home appraisal is an independent, unbiased assessment of a property’s fair market value, primarily protecting the lender’s interests. The lender typically orders it, and the buyer usually pays the fee .

What is the primary responsibility of a title company in a real estate transaction?

A title company’s primary responsibility is to ensure the property has a clear and marketable title, free of liens or legal issues, through a meticulous title search.

What are some common pitfalls homebuyers should avoid?

Common pitfalls include ignoring the budget, skipping mortgage pre-approval, focusing solely on aesthetics, neglecting the home inspection, rushing the process, hesitating to ask questions, being careless with credit, talking to only one lender, overlooking government-backed loans, and making decisions based purely on emotion.